The first case in history where humans had interactions with gold occurred in ancient Egypt around 3,000 B.C. Gold played an important role in ancient Egyptian mythology and was cherished by pharaohs and temple priests. The Egyptians also produced gold maps which described where to find gold mines and various gold deposits around the Egyptian kingdom. The Greeks viewed gold as a social status symbol and as a form of glory amongst the immortal gods and demigods. During this time period in history, mortal humans could potentially use gold as an indication of wealth, and gold was also a form of money.

Gold is also mentioned in the Bible, where Genesis 2:10-12 describes the lands of Havilah, near Eden, as a place where gold can be found. Incans, Aztecs, and numerous other civilizations also utilized, and they included it in religious ceremonies and in famous architectural designs. There’s one common trend here across all ancient civilizations: gold is a status symbol used to separate one class from another. Those who held control and power.

Marco Polo and Christopher Columbus were two explorers who were caught up in the notion that a cornucopia amount of gold could be found in far away land. Marco Polo’s book, “The Travels of Marco Polo,” told of great palaces with walls covered in gold and silver (Desjardins 2012). Spreading Christianity was a major objective of Spain, but obtaining gold and silver were high priorities too.

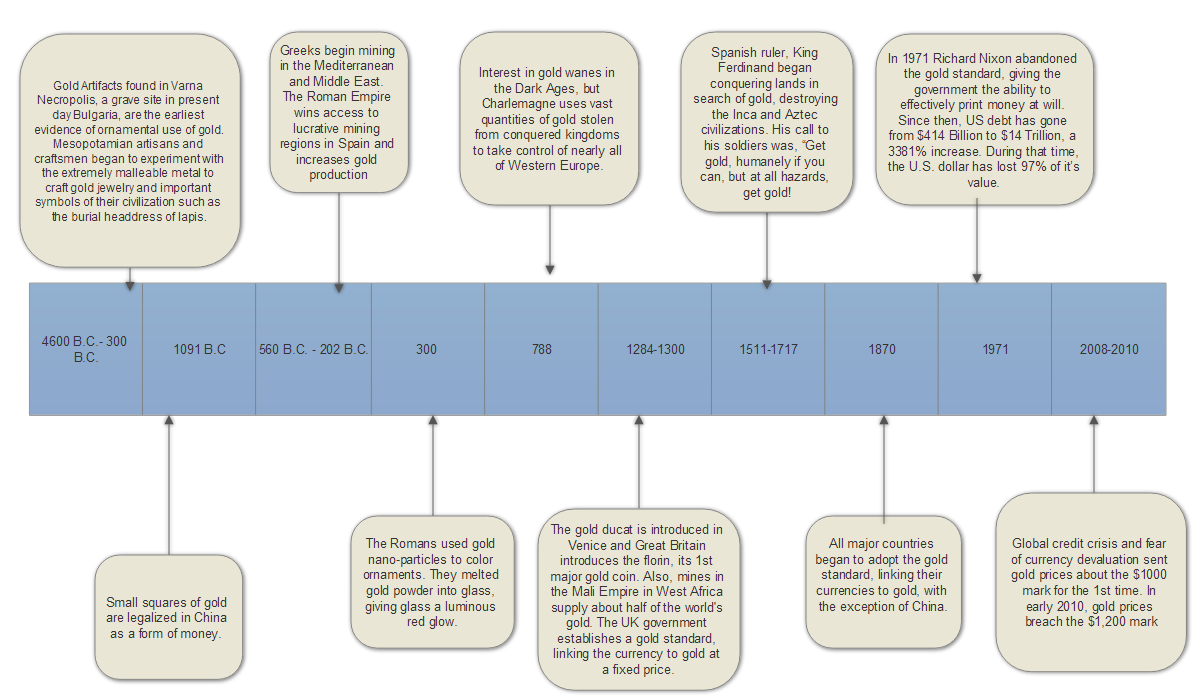

In 1511, Spanish ruler, King Ferdinand began conquering lands in search of gold, destroying the Inca and Aztec civilizations. He told his soldiers to, “Get gold, humanely if you can, but at all hazards, get gold!” Throughout the 16th century, the Spanish primarily focused on conquering Central and South America. Their goal was to search for El Dorado, a city in which gold was plentiful.

Trailer for the Road to El Dorado: Click Here

By 1870, all major countries besides China began to adopt the gold standard, which linked their currencies to gold. Countries fixed the value of their currencies in terms of a specified amount of gold. Domestic currencies were freely convertible into gold at the fixed price and there was no restriction on the import or export of gold. Since each currency was fixed in terms of gold, exchange rates between different currencies were also fixed. This guaranteed that the government would redeem any amount of paper money for its value in gold. This meant transactions no longer had to be done with heavy gold bullion or coins. Paper currency now had guaranteed value tied to something real. In 1873, Congress declared gold to be the official currency of the United States (Martin 2004). Also, in 1893, it was announced to the public that the gold reserves held in us federal treasury had fallen below $100 mill. The financial markets became alarmed, believing that the government couldn’t guarantee its bonds. Investors rushed to convert their bonds into gold, banks failed which led to a depression. A number of gold rushes occurred throughout the 1800s such as the California Gold rush were prospectors tried to get rich.

Once the Great Depression hit with full force, countries once again had to abandon the gold standard. When the stock market crashed in 1929, investors began trading in currencies and commodities. As the price of gold rose, people started exchanging their dollars for gold. When banks began crumbling, people began hoarding gold because they didn’t trust banks. Currently no countries still use the gold standard.